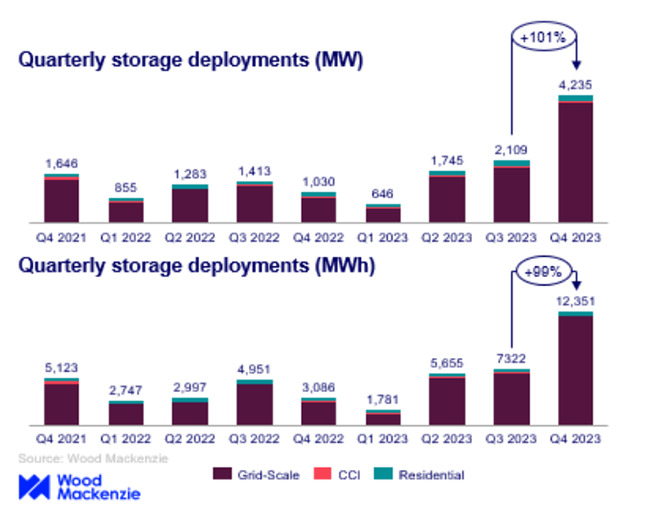

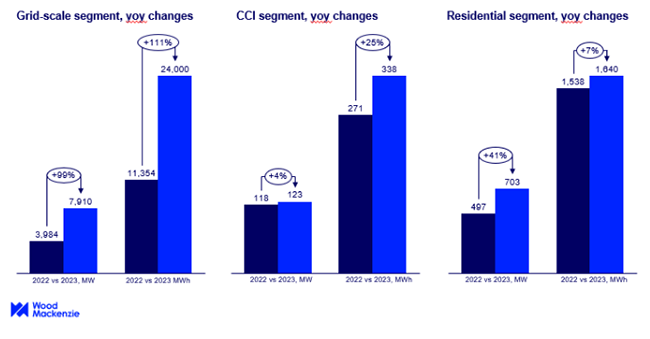

In the final quarter of 2023, the U.S. energy storage market set new deployment records across all sectors, with 4,236 MW/12,351 MWh installed during that period. This marked a 100% increase from Q3, as reported by a recent study. Notably, the grid-scale sector achieved more than 3 GW of deployment in a single quarter, nearly reaching 4 GW on its own, according to the latest U.S. Energy Storage Monitor publication by Wood Mackenzie and the American Clean Power Association (ACP). The addition of 3,983 MW in new capacity represents a 358% growth compared to the same period in 2022. John Hensley, Vice President of Markets and Policy Analysis at ACP, emphasized the industry’s significant growth momentum, stating, “The energy storage industry continues its remarkable expansion, with a record-breaking quarter contributing to a successful year for the technology.” For further information, please follow Amensolar! Residential Solar Battery, Renewable Energy Products, Solar Battery Energy Storage Systems, etc. topics. Subscribe on your favorite platform. In the U.S. residential sector, deployments reached 218.5 MW, surpassing the previous quarterly installation record of 210.9 MW from Q3 2023. While California saw market growth, Puerto Rico experienced a decline likely linked to incentive changes. Vanessa Witte, senior analyst at Wood Mackenzie’s energy storage team, highlighted the robust performance of the U.S. energy storage market in Q4 2023, attributed to improved supply chain conditions and decreasing system costs. Grid-scale installations led the quarter, exhibiting the highest quarter-on-quarter growth among segments and ending the year with a 113% increase compared to Q3 2023. California remained a leader in both MW and MWh installations, closely followed by Arizona and Texas.

The Community, Commercial, and Industrial (CCI) segment saw no significant change quarter-over-quarter, with 33.9 MW installed in Q4. Installation capacity was relatively evenly split between California, Massachusetts, and New York. As per the report, total deployments in 2023 across all sectors reached 8,735 MW and 25,978 MWh, marking an 89% increase compared to 2022. In 2023, distributed storage exceeded 2 GWh for the first time, supported by an active first quarter for the CCI segment and over 200 MW of installations in both Q3 and Q4 in the residential segment.

In the upcoming five years, the residential market is projected to continue flourishing with over 9 GW of installations. Although the cumulative installed capacity for the CCI segment is expected to be lower at 4 GW, its growth rate is more than double at 246%. Earlier this year, the U.S. Energy Information Administration (EIA) stated that U.S. battery storage capacity could surge by 89% by the end of 2024 if all planned energy storage systems become operational on schedule. Developers aim to expand U.S. battery capacity to over 30 GW by the end of 2024. As of the end of 2023, planned and operational utility-scale battery capacity in the U.S. totaled around 16 GW. Since 2021, battery storage in the U.S. has been on the rise, notably in California and Texas, where rapid growth in renewable energy is occurring. California leads with the highest installed battery storage capacity of 7.3 GW, followed by Texas with 3.2 GW. Combined, all other states have approximately 3.5 GW of installed capacity.

Post time: Mar-20-2024